The best mathematical tools to use for economic optimization include Lagrange multipliers, linear programming, calculus, and game theory. Generally, these tools help economists and businesses make informed decisions by maximizing profits, minimizing costs, and allocating resources efficiently. Furthermore, with these tools, you can achieve optimal outcomes and gain a competitive edge.

Mathematical economics uses math to solve economic problems and create new theories. Primarily, economists take the help of mathematical economics to build models that predict future economic activity. Specifically, they combine economic ideas, math techniques, and statistics to understand how the economy works and make informed decisions. In general, the advancements in computing and data analysis have made it easier to use math in economics. This has led to better ways to maximize profits, minimize costs, and solve complex economic problems. Moreover, in advanced studies, mathematical tools are used to analyze real-world economic issues and find effective solutions. If you are curious to learn how to solve optimization problems in economics, read this blog. Here, we have shared insights on the best mathematical tools you can use for economic optimization.

Real-World Applications of Economic Optimization

Optimization plays a key role in economics. It specifically helps individuals, governments, and businesses effectively use limited resources. For better understanding, let us look at some real-world examples of economic optimization here.

Maximizing Profits

Typically, businesses aim to earn the highest possible profits by using various methods. For example, airlines adjust ticket prices based on demand, seasonality, and competitor prices. Manufacturers use mathematical tools to find the perfect mix of products to make. They make this decision particularly based on their available resources, such as labor and materials. Certain digital ad platforms also use algorithms to optimize the placement of advertisements in real-time.

Minimizing Costs

The majority of companies try to reduce costs without compromising on quality. For example, Amazon optimizes delivery routes to save time and fuel. Most importantly, some businesses also reduce energy expenses by investing in efficient equipment or adjusting production schedules. Even some companies use optimization techniques to determine the ideal workforce size and shift patterns to minimize labor costs.

Allocating Resources

With the help of optimizations, businesses can effectively allocate resources. Hospitals often use management tools to optimize the use of doctors, nurses, and equipment. This, in turn, reduces patient wait times and improves overall service. Governments use optimization techniques to distribute funds among sectors like infrastructure, defense, and education. By doing so, they aim to maximize societal welfare. Even farmers use optimization techniques to boost crop yields and reduce their environmental impact. Specifically, they optimize fertilizer use, irrigation, and land management.

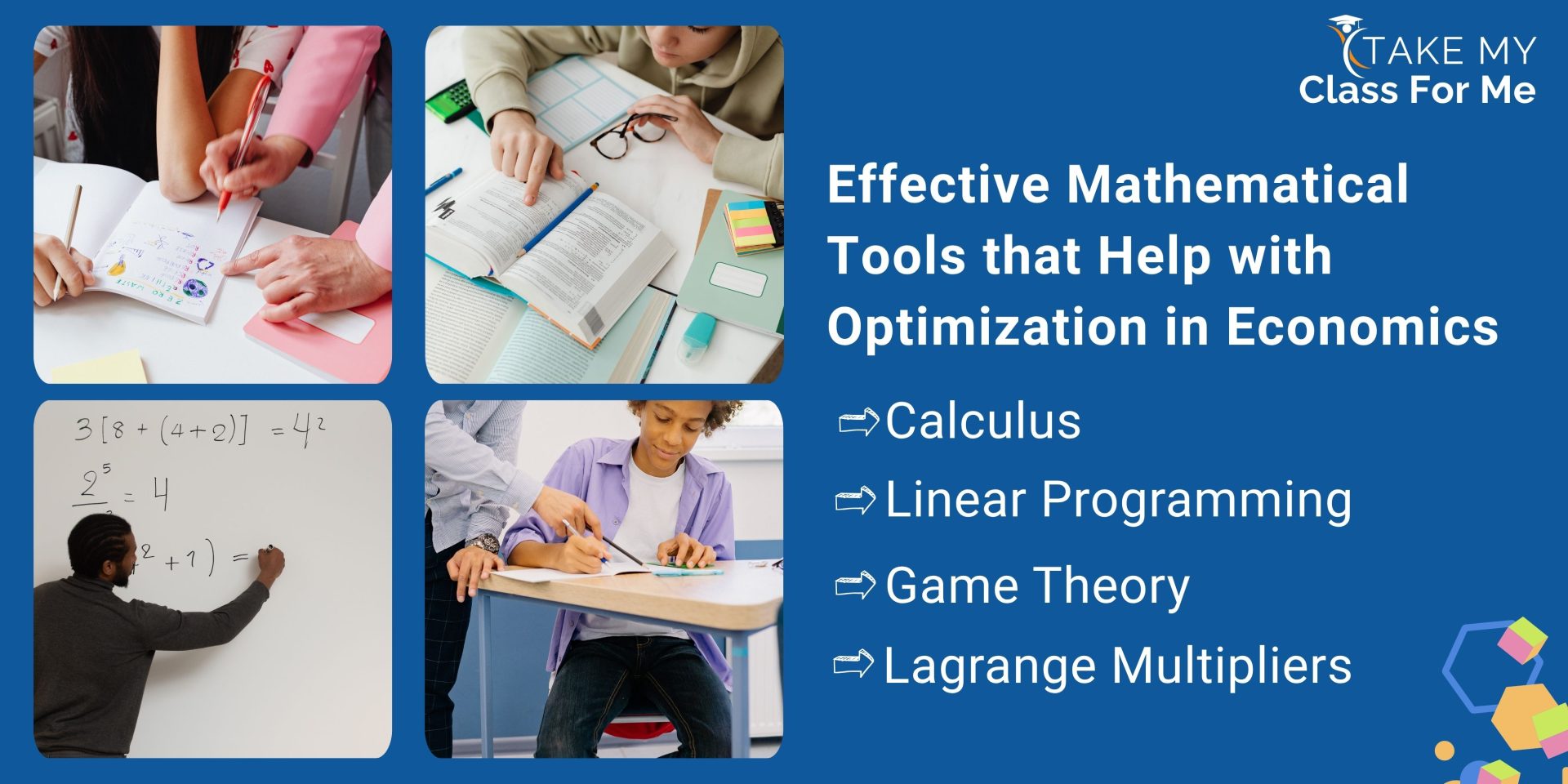

Effective Mathematical Tools that Help with Optimization in Economics

Mathematical tools are crucial for solving optimization problems in economics. Specifically, these tools will help you make informed decisions by analyzing complex economic issues in a systematic way. Typically, economic problem-solving tools, including mathematical models and computational methods, will allow you to manage challenges like maximizing profits and minimizing costs. The following are some effective mathematical tools you can use for solving optimization problems in economics

Calculus

Calculus is a branch of math that will help you understand how things change and move. It is typically divided into two parts. They are Differential Calculus and Integral Calculus. Differential calculus will show you rates of change, while integral calculus will help you understand accumulation. Differentiation will help you see how small changes impact outcomes. On the other hand, integration will help you calculate totals, like your overall cost or revenue over time.

In economics, calculus is a powerful tool for analysis. It will help you understand how changes in one thing affect another. For example, you can use calculus to find the best way to maximize your profits, minimize your costs, and analyze your revenue. Simply by using calculus, you can make better decisions and solve complex economic problems. Primarily, Calculus is a valuable tool for optimization and economic analysis that can help you achieve your goals.

Linear Programming

Linear programming (LP) is a mathematical method that can help you make the most efficient use of your limited resources. It takes into account constraints and limitations to optimize production scheduling and resource allocation. The main goal of linear programming is to increase output, reduce expenses, or achieve other objectives that matter to you.

Linear programming has many practical applications. The Simplex Method is a key tool in linear programming that you can use to solve LP problems. It is an algorithm that iteratively improves the solution until the best one is found. The Simplex Method was developed by George Dantzig to optimize resource allocation and production planning.

Game Theory

Game theory is a mathematical framework that can help you understand strategic interactions between different people or organizations. It shows how the decisions you make are influenced by the decisions of others, and vice versa. This framework is useful in both cooperative and competitive situations.

Game theory can help you make better strategic decisions, especially in dynamic and unpredictable environments. By using game theory, you can

- Predict how your competitors will set market prices

- Forecast how your competitors will react if you enter a new market

- Optimize your advertising spending and help you stand ahead from your competitors

- Determine the best bidding strategies in auctions

- Negotiate contracts with suppliers and distributors

Game theory has many real-world applications that can benefit you. For example, you can use it to analyze your competitors’ actions and make better investment decisions in the stock market. If you are involved in trade policy, game theory can help you determine the best trade agreements and tariffs. You can also use it to optimize salary negotiations and reach better agreements in labor disputes.

Lagrange Multipliers

Lagrange multipliers are a mathematical tool that can help you solve problems where you need to optimize something while considering certain limitations. In economics, you can use this tool to maximize revenue, minimize costs, and allocate resources efficiently.

For instance, you can use Lagrange multipliers to make the most of your budget by maximizing your satisfaction. You can also use it to find ways to produce goods at the lowest possible cost if you are a business owner. Additionally, if you are a company looking to maximize profits, Lagrange multipliers can help you do so while dealing with production constraints.

Conclusion

With the mathematical tools and techniques suggested in this blog, you can effectively solve optimization problems in economics. If you are unsure how to use the mathematical tools for economic optimization, then send us a ‘take my math class for me’ request. A math expert from our team will guide you in meeting your academic needs. Additionally, we also offer online economics class help to assist you in improving your understanding of the concept of optimization in economics. Get help from our subject professionals and learn how to solve optimization problems in economics with math.